Financial Freedom by 40

Introduction

Achieving financial freedom by the age of 40 may seem ambitious, but it is not just a dream reserved for the ultra-wealthy. With disciplined planning, intelligent investments, and a long-term mindset, Indian professionals in the 25–45 age group can reach this milestone well ahead of the conventional retirement age. Financial freedom doesn’t necessarily mean retiring early—it means having the choice to work because you want to, not because you have to. In this guide, we will provide you with a detailed roadmap, practical tools, and real-world strategies to help you build lasting wealth and financial independence by the age of 40.

Define What Financial Freedom Means to You

Before embarking on the journey, it is crucial to understand your destination.

- Set clear goals: Do you want to travel the world, start a business, or retire early?

- Quantify your number: Calculate the corpus you need to generate enough passive income to cover your lifestyle expenses.

- Visualize your future: Create a vision board or use tools like Notion or Trello to document your financial vision.

Use the 4% rule to estimate your financial freedom number (Annual expenses x 25).

– How It Works:

The rule is based on the idea that you can safely withdraw 4% of your investment portfolio annually, adjusted for inflation, without running out of money over a 30-year period.

– Formula:

Financial Freedom Number = Annual Expenses × 25

This means your investment corpus should be 25 times your annual living expenses.

– We Understand Using Simple Example:

Let’s say your current annual expenses are ₹10,00,000.

Financial Freedom Number = ₹10,00,000 × 25 = ₹2.5 Crores

So, you would need approximately ₹2.5 crores invested in income-generating or growth-oriented assets to be financially independent, assuming a 4% safe withdrawal rate.

– Important Notes:

- The rule assumes your corpus is invested in a diversified portfolio.

- Adjustments may be needed for inflation, tax liabilities, and healthcare costs.

- It’s a general rule, not a one-size-fits-all solution. A personalized plan is ideal.

– Calculate Your Own Financial Freedom Number form below Calculator

Financial Freedom Calculator

Master Budgeting and Expense Tracking

Budgeting is the foundation of all financial planning.

- Create a monthly budget using the 50/30/20 rule:

- 50% needs (rent, utilities, groceries)

- 30% wants (entertainment, dining out)

- 20% savings and debt repayment

- Track your expenses with tools like Money Manager, Walnut, or Excel sheets.

- Cut unnecessary expenses and optimize lifestyle costs without sacrificing joy.

Example: Switching to a more affordable data plan or avoiding daily delivery apps can save thousands monthly.

Build an Emergency Fund

Unexpected events can derail even the most robust financial plans.

- Target: Save 6–12 months of living expenses

- Where to park: Keep it in a high-interest savings account or liquid mutual fund

- Automate contributions: Set up standing instructions to build this fund gradually

Why it matters: Having an emergency buffer ensures you don’t dip into your long-term investments.

Eliminate High-Interest Debt

Debt is the biggest obstacle on the road to financial freedom.

- Prioritize: Clear credit card dues and personal loans with high interest rates (>12%) first

- Snowball or avalanche method: Choose the repayment strategy that suits your mindset

- Avoid lifestyle inflation: Don’t use loans to upgrade phones or take exotic vacations

Tip: Negotiate interest rates or consolidate debt to reduce monthly outflows.

Invest Aggressively and Wisely

Investing is the most powerful tool for wealth creation.

- Start early: The earlier you begin, the greater the power of compounding

- Asset allocation: Diversify across equity, debt, and alternate assets

- Recommended options:

- Mutual funds via SIPs

- Index funds (low-cost, passive growth)

- Direct equity (only if you can research and monitor)

- PPF and NPS for tax-saving and retirement

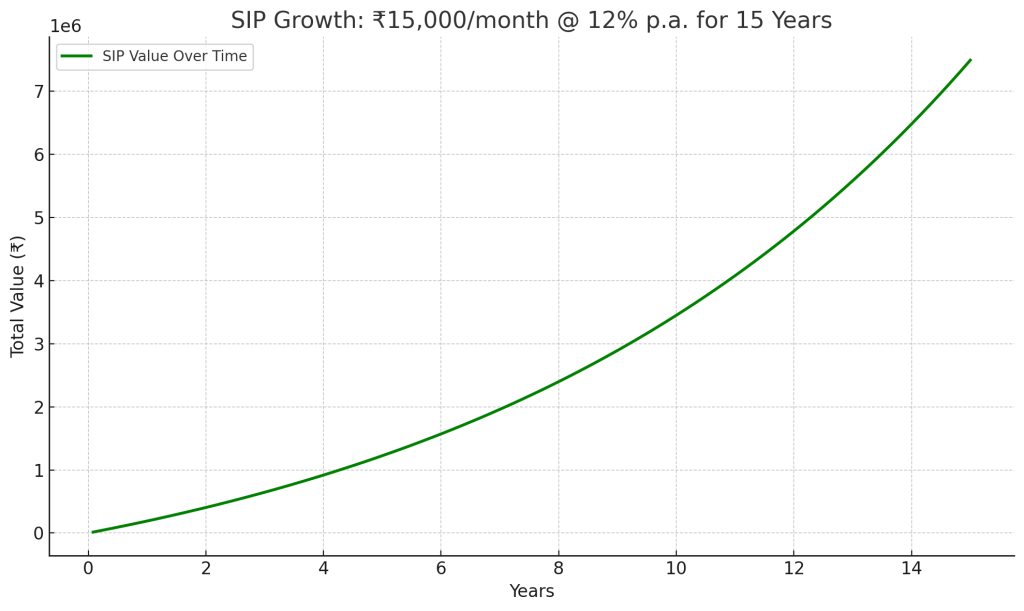

Example: A monthly SIP of Rs. 15,000 growing at 12% p.a. can accumulate over Rs. 1 crore in 15 years.

Optimize for Tax Efficiency

Every rupee saved in taxes is a rupee earned.

- Utilize Sections 80C, 80D, and 24(b) for deductions

- Choose tax-friendly investments: ELSS, NPS, and ULIPs

- Invest via HUF or use spousal income to optimize taxation

Bonus Tip: Consult a CA annually to restructure finances for minimal tax liability.

Protect Your Wealth with Insurance

Insurance is not an investment—it’s protection.

- Life Insurance: Buy a term plan with coverage of at least 10–15x your annual income

- Health Insurance: Opt for a family floater plan; consider super top-up plans

- Critical Illness & Disability: These can protect your wealth from unexpected health crises

Reminder: Never mix insurance and investment—avoid endowment and money-back policies.

Regularly Review and Rebalance

Financial plans are not "set and forget."

- Review goals annually and adjust for life changes (marriage, kids, job switch)

- Rebalance your portfolio to maintain asset allocation

- Track net worth and compare it against your freedom goal

Cultivate the Right Mindset

Wealth-building is 80% behavior and 20% math.

- Practice delayed gratification and avoid lifestyle creep

- Read books: "Rich Dad Poor Dad," "The Psychology of Money"

- Surround yourself with financially-aware peers

Quote to Live By

“If you don’t find a way to make money while you sleep, you will work until you die.”

– Warren Buffett

“If you don’t find a way to make money while you sleep, you will work until you die.” – Warren Buffett

Conclusion

Financial freedom by 40 is achievable with a clear plan, consistent action, and smart decision-making. It requires not just saving more, but also earning more, investing wisely, and protecting what you build. Whether you're just starting out in your 20s or are mid-career in your 30s, the time to act is now.

At DreamFunds.in, we specialize in crafting personalized financial plans that align with your life goals. Explore our tools, resources, and advisory services to take the next big step toward your financial independence. Your journey to freedom begins with one informed decision—make it today.

Leave a Reply