Unlocking Financial Freedom with SWP (Systematic Withdrawal Plan) can help investors achieve financial independence by providing a steady income stream from mutual fund investments. It highlights SWP as a smart, strategic approach to withdrawing money while allowing the remaining corpus to grow. The phrase “Unlocking Financial Freedom” appeals to individuals planning for retirement, passive income, or financial stability, making it engaging and aspirational.

Introduction to Systematic Withdrawal Plan (SWP)

A Systematic Withdrawal Plan (SWP) is a structured way to withdraw money from mutual fund investments at regular intervals while allowing the remaining corpus to continue growing. It is designed for investors who seek a steady income stream without liquidating their entire investment. Unlike lump-sum withdrawals, SWP offers flexibility, tax efficiency, and financial stability, making it ideal for retirees, those planning passive income, or individuals managing expenses systematically. By strategically redeeming units, investors can maintain cash flow while benefiting from market growth. SWP is a smart financial tool that ensures disciplined withdrawals while keeping wealth intact for long-term goals.

- Briefly define SWP: A strategy that allows investors to withdraw a fixed amount from their mutual fund investments at regular intervals.

- Compare it with other withdrawal strategies (e.g., lump sum, dividends).

- Explain why SWP is useful for financial planning, retirement income, or achieving financial goals.

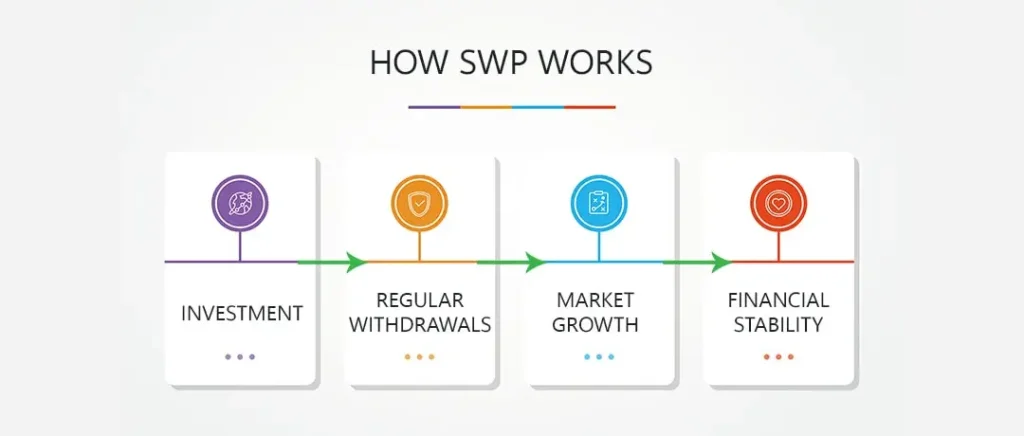

2. How SWP Works in Mutual Fund Investments

A Systematic Withdrawal Plan (SWP) works by allowing investors to withdraw a fixed amount from their mutual fund investments at regular intervals, such as monthly, quarterly, or annually. When an SWP is set up, mutual fund units are redeemed systematically to generate the required cash flow, while the remaining corpus continues to grow based on market performance. Unlike lump-sum withdrawals, SWP ensures a steady income while optimizing tax benefits, as only the capital gains portion is taxed. It provides financial stability, making it a popular choice for retirees and those seeking passive income without disrupting their long-term investments.

- Explain the mechanics of SWP:

- Investor chooses a mutual fund and sets a withdrawal amount and frequency.

- Units are redeemed systematically to generate cash flow.

- Remaining investment continues to grow based on market performance.

- Highlight tax efficiency:

- Only capital gains are taxed (potential tax benefits over fixed deposits).

- Lower tax liability under long-term capital gains (LTCG) compared to traditional income sources.

3. Benefits of Starting Early with SWP

Starting an SWP (Systematic Withdrawal Plan) early offers significant financial advantages, primarily due to the power of compounding and long-term wealth accumulation. By investing in mutual funds early and setting up an SWP later, investors can build a substantial corpus that sustains steady withdrawals without depleting the principal quickly. Early planning allows the investment to grow over time, making withdrawals more sustainable and tax-efficient. It also provides flexibility to adjust withdrawal amounts as financial needs evolve. Whether for retirement, passive income, or future financial goals, starting early with SWP ensures financial security and maximizes returns in the long run.

- Power of Compounding: The longer the investment period, the greater the wealth accumulation.

- Flexibility: Investors can adjust the withdrawal amount as per financial needs.

- Market Protection: SWP mitigates risks of market volatility compared to lump-sum withdrawals.

- Tax Efficiency: Lower tax burden as compared to traditional interest income.

4. Real-Life Example & Calculation

Scenario: Retirement Planning with SWP

Consider an investor who invests ₹50 lakh in a balanced mutual fund with an average annual return of 10%. They set up an SWP of ₹30,000 per month, ensuring a steady income while keeping the investment growing. Over 20 years, they withdraw ₹72 lakh in total, but due to compounding, the remaining corpus still holds significant value. Compared to a fixed deposit, where the capital depletes over time, an SWP allows withdrawals while benefiting from market appreciation. This approach makes SWP ideal for retirees or individuals seeking passive income without exhausting their investment, ensuring long-term financial stability.

- Investment: ₹50 lakh in a balanced mutual fund with an average return of 10% per annum.

- SWP Setup: ₹30,000 monthly withdrawal.

- Outcome:

- Monthly cash flow while keeping investment intact.

- After 20 years, even after withdrawals, a significant corpus remains due to compounding.

Alternative Scenario: Early Planning for Passive Income

- Investing ₹10,000 per month in mutual funds for 20 years at 12% returns.

- Accumulated corpus: ₹1 crore+.

- Setting up SWP post-retirement ensures a steady monthly income without depleting the entire corpus.

5. SWP vs. Dividend and Fixed Deposit Withdrawals

A Systematic Withdrawal Plan (SWP), dividend payouts, and fixed deposit withdrawals are three common ways to generate regular income, but SWP offers distinct advantages. Unlike dividends, which fluctuate based on company profits, SWP provides a fixed, predictable cash flow. Compared to fixed deposits (FDs), SWP is more tax-efficient since only capital gains are taxed, whereas FD interest is fully taxable. Additionally, SWP allows the remaining investment to grow, unlike FDs, which provide fixed returns with no market appreciation. This makes SWP a superior choice for investors seeking steady income, flexibility, and long-term financial growth without compromising liquidity.

| Feature | SWP | Dividend | Fixed Deposit |

|---|---|---|---|

| Steady Income | ✅ | ❌ (Fluctuates) | ✅ |

| Market Growth Benefit | ✅ | ✅ | ❌ |

| Tax Efficiency | ✅ | ❌ (Taxable) | ❌ (Taxable) |

| Flexibility | ✅ | ❌ | ❌ |

6. How to Set Up an SWP with Dream Funds

Setting up an SWP with Dream Funds is simple and customized to fit your financial goals. First, choose a suitable mutual fund based on your risk tolerance and income needs. Next, decide on the withdrawal amount and frequency—whether monthly, quarterly, or annually. Our experts at Dream Funds help you select tax-efficient funds to optimize returns. Once the SWP is activated, a fixed amount is withdrawn while the remaining corpus continues to grow. You can modify or stop the SWP anytime, offering complete flexibility. Start your SWP journey with Dream Funds today and secure a steady income stream effortlessly!

- Choose the right mutual fund based on financial goals.

- Decide on a withdrawal amount based on expenses.

- Select the right frequency (monthly, quarterly).

- Start with Dream Funds’ expert guidance for optimal fund selection and tax planning.

Frequently Asked Question

Can I start an SWP with any mutual fund?

Yes, SWP can be set up with most mutual funds, but it is recommended to choose debt, balanced, or hybrid funds for stable returns. Equity funds can also be used, but they are subject to higher market fluctuations.

What happens if the market declines during an SWP?

During market downturns, more mutual fund units will be redeemed to meet the withdrawal amount. However, long-term investment in well-chosen funds can help mitigate risks and sustain the corpus over time.

Is SWP better than keeping money in a savings account for monthly withdrawals?

Yes, SWP offers higher returns compared to a savings account, which provides minimal interest. Additionally, SWP is more tax-efficient and allows your investment to grow over time while providing steady cash flow.

Can I change the withdrawal amount in an SWP?

Yes, most mutual fund houses allow investors to increase, decrease, or stop the SWP amount based on their financial needs. This flexibility makes it an excellent tool for financial planning.

What is the minimum investment required to start an SWP?

The minimum investment varies across mutual fund houses, but typically, investors need ₹50,000 to ₹1,00,000 as an initial corpus to start an SWP. Some funds may allow SWP with a lower amount, depending on the fund type.

Leave a Reply